Transparency Market Research

Organic Pet Food Market - Global Industry Analysis and Forecast 2025

Organic pet food is a natural food for pet which has to meet the US Department of Agriculture (USDA) regulations described for organic label. Organic pet food has health benefits on animals such as reduction in skin allergies and aliments, fewer digestive disorders, better overall health, quality life etc. Changing family structures and lifestyles lead to smaller pets, are factors fueling the growth of ownership of pets globally, thus, market demand for organic pet food is rising globally. Increasing consumer awareness about animal health and pet humanization is resulting in growing market demand for organic pet foods. Organic pet food market is segmented on the basis of type of animals and distribution channels. Organic pet food available for dog, cat, birds, ducks etc. is different as it contains different quantities of ingredients as required by specific animal. Online retailers are offering organic pet food products available due to increasing demand globally.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=21662

Market Segmentation: Organic Pet Food

The organic pet food market is segmented on the basis of animal type as dog, cat, duck, bird and other animal pet foods. As a result of increasing trend of nuclear families and increasing demand for small pets is growing organic pet food global market. As a result of increasing trend of nuclear families and increasing demand for small pets are factors fueling growth of the global market for organic pet foods global market. There is a broad global trend towards small pets, not only cats and small dogs, but also small mammals in some markets. Thus, cat and dog organic pet foods market segments are expected to grow rapidly over the forecast period.

The organic pet foods market is further segmented on the basis of distribution channel as supermarket/ hypermarket, retail stores, online stores, specialized pet shops etc. As a result of increasing trend of pet humanization is a factor fueling demand for organic pet foods in supermarket/ hypermarket. To cater to increasing demand for organic pet foods retail shops and online stores are also gaining interest and driving the market for organic pet foods. Specialized pet shops are gaining popularity and preference by high profile consumers due to availability of various branded, natural organic pet foods products and varieties for all pet animals.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/increasing-popularity-of-dark-chocolates-to-spur-growth-of-cocoa-fiber-market-valuation-to-rise-to-us747-mn-by-2030-finds-tmr-301070098.html

Global Organic Pet Food Market: Regional Outlook

Depending on geographic regions global organic pet food market is segmented into five key regions: North America, Latin America, Europe, Middle East and Africa and Asia Pacific. North America have maximum share in organic pet food in global market followed by Europe due to increasing trend of pet ownership globally. North America is the largest market for Organic pet foods and grabs higher market share in global market. Increasing trend of ownership of pet in Europe is growing demand for Organic pet foods. Asia Pacific is expected to grow at highest CAGR over the forecast period. Organic pet foods market is gaining interest in global market due to its health benefits associated in animals.

Global Organic Pet Food Market: Drivers and Trends

Organic pet food demand is increasing due to changing life style in different countries. Perception of consumers towards health of pet is increasing, resulting in growing demand for organic pet food market. Increasing trend of nuclear family is one of the factor responsible for growth of organic pet food market. Increasing awareness of pet health is one of the key driver for rise in market for organic pet food. Adoption of pet is increasing globally in turn increasing demand for organic pet food. Advertisements and pet health awareness drives are increasing and endorsements done by celebrities is driving the global organic pet food market.

Changing consumer’s perception towards health of pet is resulting in growing demand for organic and natural pet foods market. Increasing trend of nuclear family is one of the factor responsible for growth of pet foods market in turn organic pet food. Increasing awareness of pet health is one of the key driver for rise in market demand for organic pet foods. Adoption and humanization of pet is increasing globally in turn increasing demand for organic pet foods. Advertisements and pet health awareness drives are increasing and endorsements done by celebrities is another factor fueling the growth of global organic pet foods market. Increasing disposable income and changing consumer life style are other factors driving demand and growth of the global organic pet food market.

Request For the Customization - https://www.transparencymarketresearch.com/sample/sample.php?flag=CR&rep_id=21662

Global Organic Pet Food Market: Restrains

Organic pet food has restraints such as supply issue, high prices, organic regulations etc. Suppliers in this market are not yet established which makes it difficult in supplying the organic products. Organic products have higher prices due to high quality ingredients used in preparation of organic pet foods. Organic regulations are very complicated which makes it difficult for manufacturers to get the natural label claim for their products. All these factors affects penetration of organic pet food market in mass outlets.

Global Organic Pet Food: Key Players

Some of the key players identified across the value chain of the global organic pet food market include KLN Family Brands, Halo Purely for Pets, Newman's Own, PetGuard, Nature’s Variety, Party Animal Inc., Blue Buffalo Co., Ltd., Solid Gold Pet, LLC, Mars, Incorporated, Grandma Lucy’s LLC, Merrick Pet Care etc.

The report offers a comprehensive evaluation of the market. It does so via in-depth qualitative insights, historical data, and verifiable projections about market size. The projections featured in the report have been derived using proven research methodologies and assumptions. By doing so, the research report serves as a repository of analysis and information for every facet of the market, including but not limited to: Regional markets, technology, types, and applications.

Request for covid19 Impact Analysis -https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=21662

Papain Market - Global Industry Analysis, Size, Share, Growth, Trends, and Forecast 2027

Global Papain Market: Overview

Papain is a natural cysteine proteolytic enzyme present in mountain papaya (Vasconcellea cundinamarcensis) and papaya (Carica papaya). It is native to Latin America and is also called as papaya proteinase I. It is used to tenderize meat eaten as it breaks down tough meat fibers. Papain is an active component in powder form for meat tenderizers and has a huge demand in the global market. Papain also used in chemo-mechanical dental caries removal gel known as Papacarie, as a tooth whitener in mint sweets and toothpaste, to clean up dead tissue in chronic wounds, as a component of many enzymatic debriding preparations, and cell dissociation in cell culture preparations. The end-use industries of the papain include leather, food & beverages, detergents, cosmetic, tanning, optical, photographic, textile, and pharmaceutical. The North America papain market accounts for relatively high revenue share, followed by Western Europe papain market over the forecast period, attributed to relatively strong demand for papain and broad availability of raw material in the regions.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=21296

Global Papain Market: Dynamics

Some of the important factor fueling the growth of global papain market include rising health concern among the consumers, high demand for meat tenderizers, and increasing demand for natural enzymes. To counter the same, papain market players are investing in research and development and production of papain to meet the regulatory specification with increasing demand. Some macroeconomic factors making a positive impact on global papain market includes increasing population, the rapid rate of urbanization, and growing domestic income. The trend identified in the global papain market is mergers and acquisitions between papain producers and papaya suppliers. The company manufacturing papain products has a significant opportunity in regions such as North America, Europe, and Asia Pacific, attributed to high demand for natural enzymes and growing health consciousness among a large number of population. Companies have a significant opportunity in global papain market through collaboration with raw material supplier i.e. papaya vendor and through backward integration in the market as a raw material is a key factor for the market.

Global Papain Market: Segmentation

Global papain market is segmented by end-use industry and by region. By end-use industry, the global papain market is sub-segmented as food & beverages, cosmetic, textile, pharmaceutical, other industries such as detergents, tanning, optical, photographic, etc. Among these, the pharmaceutical segment is expected to contribute to the significant revenue share with a relatively high growth rate over the forecast period in global papain market. A pharmaceutical segment follows food & beverages segment with a relatively high growth rate concerning both value and volume in the global papain market.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/coconut-syrup-market-to-reach-valuation-of-us-354-mn-by-2029-demand-for-organic-food-in-us-shall-propel-the-dominance-of-north-america-in-global-market-finds-tmr-301027365.html

Based on the end-use industry, the global papain market is segmented into:

Food & Beverages Industries

Cosmetic Industries

Textile Industries

Pharmaceutical Industries

Other Industries (detergents, tanning, optical, photographic, etc.)

Global Papain Market: Regional Overview

By geographies, the global papain market is segmented into seven regions -- North America, Western Europe, Asia-Pacific except Japan, Eastern Europe, Latin America, the Middle East & Africa, and Japan. Among the regions, North America accounts for a relatively high share of the global papain market in terms of value, owing to strong demand for natural enzymes particularly in the U.S. Western Europe is followed by North America in global papain market, attributed to high demand for meat tenderizers across the region. Eastern Europe and Japan also accounts for significant value share in the global papain market. The Asia-Pacific is expected to register relatively high growth rate in the global papain market over the forecast period, owing to the robust growth of pharmaceutical industry due to rapidly growing population across the region particularly in the countries such as China and India. Latin America and Middle East Africa is expected to have relatively high opportunity for papain market players, attributed to the rapid rate of industrial growth and high demand for meat products. Overall, the outlook for the global papain market will have a positive growth over the forecast period.

Request for Custom Research at - https://www.transparencymarketresearch.com/sample/sample.php?flag=CR&rep_id=21296

Global Papain Market: Key Players

Few players of papain market include Senthil Papain and Food Products (P) Ltd., FRUZYME BIO TECH INDIA PVT LTD, Shri Ganesh Industrial Enzymes, Aumgene Biosciences, Shree Sai Agros, Parchem fine & specialty chemicals, Ultra Bio-Logics Inc., LGM Pharma, Chemos GmbH, Beckmann-Kenko GmbH, and AXO Industry SA.

The report offers a comprehensive evaluation of the market. It does so via in-depth qualitative insights, historical data, and verifiable projections about market size. The projections featured in the report have been derived using proven research methodologies and assumptions. By doing so, the research report serves as a repository of analysis and information for every facet of the market, including but not limited to: Regional markets, technology, types, and applications.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=21296

Liquid Metal Battery Market - Global Industry Analysis, Size, Share, Growth, Trends, and Forecast 2025

Efficiency and reliability of energy transmission and storage is dependent on the storage capacity of the battery. This is applicable to all systems, ranging from small personal devices to power grids. Batteries are used to supply power to portable devices, to fuel vehicles, and to cause disruptions in the working of electric grids. However, despite the high applicability of batteries, technological advances in the battery industry in meeting the demand for power in the modern world have been slow-paced.

A noteworthy innovation in the battery industry is the pioneering research on liquid-metal rechargeable batteries conducted by Professor Donald Sadoway at the Massachusetts Institute of Technology. The research included application of magnesium-antimony (Mg-Sb) and lead-antimony (Pb-Sb) in the experiments at MIT. In the experiment, electrode and electrolyte layers are heated until they turn into liquid and segregate due to density and immiscibility. Liquid metal batteries have longer lifespans than conventional batteries.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=38813

The technology for liquid metal batteries was first proposed in 2009. It was based on the separation of magnesium and antimony by molten salt. The selection of magnesium and antimony at negative and positive electrodes, respectively, was done primarily due to their low cost. Moreover, magnesium exhibited low solubility in molten-salt electrolyte, whereas, antimony was anticipated to discharge higher voltage.

Based on metal composition in battery, the liquid metal battery market can be segmented into Mg-Sb battery, Pb-Sb battery, and Na-S battery. Sodium-sulfur (Na-S) batteries are partially molten-metal batteries. They can be used for storing energy for renewable applications, load leveling, or providing backup source. Raw materials required for producing Na-S batteries are relatively inexpensive; they are also abundantly available. However, the lifespan of Na-S battery is short due to degradation caused by the corrosive nature of its active ingredients viz. sodium and sulfur. Furthermore, usage of Na-S batteries has been limited to large-sized applications.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/global-solar-street-lighting-market-to-reach-a-valuation-of-us-12-54-bn-by-2027-the-renewable-energy-movement-to-drive-solar-street-lighting-market-finds-tmr-301028795.html

In 2010, commercialization of the liquid metal battery technology invented at MIT was carried out through the Liquid Metal Battery Corporation (LMBC). The company was later renamed as Ambri in 2012. Ambri launched its commercialized liquid metal battery technology in 2016. Liquid metal batteries are projected to have a lifespan of more than 15 years with no degradation in performance. These batteries can be custom designed in order to meet specific needs.

Development of liquid metal battery is an innovative approach for solving problems in grid-scale electricity storage. Integration of renewable resources into power grid can be improved with the capabilities of liquid metal batteries. Moreover, liquid metal batteries are perceived to improve the reliability of an aging grid. They are also likely to counterbalance the requirement of additional transmission, generation, and distribution assets in a grid system. The end-user market of liquid metal battery is fairly competitive as constant innovations targeting utility-scale energy storage applications are underway.

Request For the Customization - https://www.transparencymarketresearch.com/sample/sample.php?flag=CR&rep_id=38813

The liquid metal battery utilizes three liquid layers as electroactive components. These components comprise liquid metal positive electrode, a fused salt electrolyte, and a liquid metal negative electrode. Due to the difference in their density and immiscible properties, these three liquid layers can float on top of each other. This characteristic, along with the usage of inexpensive materials, fosters low assembly cost of liquid metal batteries.

Liquid metal batteries can overcome mechanism failure generally faced by solid-state battery components. This has the potential to elongate the lifespan of the device. Ongoing research in this field comprises several engineering challenges and scientific topics such as computational thermal modeling, fundamental thermodynamic measurements of candidate electrode couples, electrochemical studies of molten salt electrolytes, long term corrosion and lifespan testing, and scaling up the design to build larger single-cells.

Key players operating in the liquid metal battery market include Ambri Inc., EnerVault, Aquion, and Pellion Technologies.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=38813

The report offers a comprehensive evaluation of the market. It does so via in-depth qualitative insights, historical data, and verifiable projections about market size. The projections featured in the report have been derived using proven research methodologies and assumptions. By doing so, the research report serves as a repository of analysis and information for every facet of the market, including but not limited to: Regional markets, technology, types, and applications.

FGD Gypsum Market - Global Industry Analysis & Forecast 2025

FGD Gypsum Market: Overview

FGD Gypsum is a synthetic product produced at electric power plants from flue gas desulfurization (FGD) systems. In this process, sulfur is removed from combustion gases using scrubbers. Scrubbers are the substances used in chemical reactions to produce other substances. Scrubbers used for the production of FGD gypsum uses limestone or lime reagents. The process of manufacturing FGD Gypsum is eco-friendly and provides ecologically sound and sustainable source of pure gypsum.

FGD gypsum finds its applications in various segments including glass making, water treatment, cement production, mining applications, highway construction, gypsum panel products, and agriculture. In agriculture, FGD gypsum can be used as soil amendment in various hydrogeological and soil conditions. It is used for water infiltration and storage and as a nutrition source for crops. Furthermore, it can be used as a conditioner that enhances physical properties of soil. Furthermore, it helps to reduce sediment and nutrient movement to surface water. It provides an effective method of industrial material recycling and soil conservation, and hence is supported by various governments around the world.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=26819

In the construction industry, FGD gypsum is used for the manufacturing of plaster of Paris, cement, and wallboard. The increasing demand for these applications are expected to boost the global market of FGD gypsum. Furthermore, FGD gypsum is recyclable and is used by the prominent manufacturers. Plaster of Paris is used for creating sculptures, structures, and decorative panels. Its demand is expected to grow, further fuelling the demand for FGD gypsum. FGD gypsum is also used in the mining industry for the applications such as subsidence control in underground mines, alkaline amendment to neutralize acid-producing rock, as a barrier to acid mine drainage formation, and as an encapsulation or neutralization of acid-producing materials

FGD gypsum, also known as synthetic gypsum, is manufactured through the process of flue gas desulfurization. Flue gas desulfurization is a technology used to eliminate sulfur dioxide (SO2) from exhaust flue gases of fossil-fuel power plants. The process keeps the air clean and provides sustainable and ecologically sound source of pure gypsum. The product is created while carrying out various industrial processes. Industrial production of phosphoric acid, titanium, hydrofluoric acid, and citric acid helps produce phosphogypsum, titanogypsum, fluorogypsum, and citrogypsum, respectively, as their by-product. The product manufactured is an environmentally friendly, highly sustainable and of high quality. The usage of the synthetic gypsum form FGD is expected to increase as more coal fired power plants convert their desulphurization processes to produce commercial gypsum. Increase in construction of wallboard plants near these power plants is also anticipated to boost the usage of FGD gypsum.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/inks-market-to-reach-a-valuation-of-us-21-2-bn-by-2027-increasing-demand-from-packaging-industry-to-offer-lucrative-growth-opportunities-observes-tmr-300999345.html

FGD gypsum is used in various industries such as agriculture and construction based upon its usage. In terms of application, the FGD gypsum market can be segmented into wallboard, cement, plaster of Paris, fertilizers, and others. FGD gypsum is primarily used in the form of wallboards and plasterboards in the construction industry. FGD gypsum is also added to cement as filler or retarder. Plaster of Paris is utilized to create decorative panels, structures, and sculptures for the building & construction industry. FGD gypsum is a versatile mineral and is employed as a fertilizer in agriculture. It is primarily added as sulfur or calcium fertilizer. Additionally, gypsum is utilized as soil conditioner; it helps retain water. FGD gypsum is also used in ornaments and other decorative items.

Growth in the construction industry in Asia Pacific, North America, and Europe is anticipated to boost the global FGD gypsum market in the near future. Demand for gypsum is high in the construction industry due to wide applications in wallboard, cement, and plaster of Paris. FGD gypsum is recyclable; this makes it the first choice of material in the construction industry. The construction industry in Europe is significantly strong. It accounts for 10% share of the GDP of European Union. The construction industry in Europe is estimated to expand at a steady rate of 3% till 2020. The construction industry is significantly strong in Western Europe as compared to its counterpart in Eastern Europe. Furthermore, the European Union is focusing on energy efficient and green buildings plans. The region has developed a strong regulatory framework to achieve sustainable construction. These initiatives are likely to fuel the demand for gypsum wallboards and plasterboards in the construction sector in Europe. FGD gypsum boards are more energy-efficient and provide greener solutions than cement and concrete structures. Increase in population along with improvement in the standard of living in Asia Pacific is boosting the market in the region. In developing nations such as China and India, the demand for FGD gypsum is higher due to the development of industries and growth in the construction industry.

Ask for Discount on Premium Research Report With Complete TOC at - https://www.transparencymarketresearch.com/sample/sample.php?flag=D&rep_id=26819

The FGD gypsum market is highly consolidated; seven to eight manufacturers account for more than 80% the share globally. However, the rest (20%) of the market is relatively fragmented. Key manufacturers operating in the gypsum market include EDF Energy, E.ON UK Plc, Scottish & Southern Energy Plc, Rugeley Power Ltd., Drax Power Ltd., Eggborough Power Ltd., ?EZ Energetické produkty, s.r.o., STEAG Power Minerals GmbH, VGB PowerTech e.V., and BauMineral GmbH.

The report offers a comprehensive evaluation of the market. It does so via in-depth qualitative insights, historical data, and verifiable projections about market size. The projections featured in the report have been derived using proven research methodologies and assumptions. By doing so, the research report serves as a repository of analysis and information for every facet of the market, including but not limited to: Regional markets, technology, types, and applications.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=26819

Solar Cooling Market - Global Industry Analysis and Forecast 2025

Solar cooling is also known as air-conditioning that utilizes solar power. This can be done through solar thermal energy conversion, photovoltaic conversion, and passive solar building design. Solar cooling provides zero-energy and energy-plus design of buildings. Lighting and air-conditioning accounts for more than 50% of the overall electricity consumption in the industrial sector. Thus, industry needs new solutions to reduce the electricity demand of conventional A/C systems. This would drive the solar cooling market during the forecast period. Increasing demand for refrigeration and air-conditioning has led to increase in electricity demand across the globe. This would also drive the solar cooling market in the near future, as solar thermal cooling can reduce the conventional electric A/C loads. Key challenge before the market is to reduce system costs.

Based on end-use, the solar cooling market has been segmented into commercial, residential, and industrial. Air-conditioning is a constantly growing industry and is likely to expand during the forecast period. Renewable energy is now a lucrative industry and it is projected to expand tremendously across the globe in the near future. Renewable energy includes solar cooling application and solar thermal energy application which are growing tremendously. The increasing demand for renewable energy is estimated to boost the solar cooling market during the forecast period.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=26663

Based on solar cooling system, the solar cooling market has been divided into desiccant systems and absorption systems. In a desiccant system, air passes through a drying material such as silica gel, which absorbs moisture from the air and makes the air more comfortable. The desiccant is regenerated by using solar heat. Absorption chiller systems, the most common solar cooling systems, use solar water heating collectors and a thermal–chemical absorption process to attain air-conditioning without using the electricity.

Geographically, the global solar cooling market has been segmented into North America, Latin America, Europe, Asia Pacific, and Middle East & Africa. Asia Pacific is one of the key consumers of solar cooling systems. Developing economies such as China witness significant growth in the industrialization. Moreover, changing lifestyles also play a role in propelling the solar air-conditioning market. Asia Pacific is estimated to be a rapidly expanding market for solar cooling in the next few years, due to growing economy of the region and presence of developing countries such as China and India in Asia Pacific.

More Trending Reports by Transparency Market Research - https://www.prnewswire.co.uk/news-releases/stationary-fuel-cell-market-to-attain-revenue-of-us-8-5-bn-by-2027-clean-energy-demand-to-drive-stationary-fuel-cell-market-from-2019-to-2027-tmr-846134488.html

Stringent government regulations and incentives have been fueling the solar cooling market in Italy for the last few years. The high budget available for a national incentive scheme called Conto Termico 2.0 has made several manufacturers and service providers positive about the solar cooling market in Italy. The market in the country is likely to expand during the forecast period. China holds a major share of the solar cooling market across the globe. In 2016, two large solar thermal cooling systems were installed in China. One of them was a 23-kW Yazaki absorption system and the other one was a newly developed, 50-kW, variable-effect absorption chiller driven by a Fresnel collector. Jordan (MEA) is witnessing rapid increase in demand for solar cooling, as the German Agency for International Cooperation is expected to initiate a solar cooling project in industrial and commercial sectors in Jordan.

Request For the Customization - https://www.transparencymarketresearch.com/sample/sample.php?flag=CR&rep_id=26663

The solar cooling includes both solar PV solutions and solar thermal market in near future across globe. However, PV cooling technologies are more economical than grid-driven electric chillers at cooling loads of 100 KWc. On the other hand, solar thermal cooling should be used for 1 MWc cooling. Europe is the second-largest market for solar cooling across the globe, as Germany is one of the key markets for solar cooling or solar air conditioning.

Key players operating in the global solar cooling market include SolXenergy, LLC, Honeywell International Inc., SorTech AG, SM Solar Pvt. Ltd., and Arka Technologies.

The report offers a comprehensive evaluation of the market. It does so via in-depth qualitative insights, historical data, and verifiable projections about market size. The projections featured in the report have been derived using proven research methodologies and assumptions. By doing so, the research report serves as a repository of analysis and information for every facet of the market, including but not limited to: Regional markets, technology, types, and applications.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=26663

Hemp-based Food Market - Global Industry Analysis and Forecast 2024

Hemp-based food products have gained immense popularity due to their easy digestibility by dint of being free from gluten, allergens, genetically modified organisms (GMO), lactose, phytoestrogen, and pesticides. Hemp is a good source of fiber and vitamins &minerals including magnesium, vitamin E, zinc, and iron. Consumption of hemp-based food products aids the maintenance of a healthy digestive system which further drives the overall market across developed regions such as North America and Europe. Hemp seeds are a highly nutritious source of protein and are being increasingly used in packaged foods such as granola bars, pretzels, bread, and cereals. The global hemp-based food market is divided by ingredients into the protein, oil, and seed categories. Among these, hemp seeds dominated the global market in 2015 and are expected to retain its leading position over the forecast period. Their growing usage in various foods such asnut butter, corn chips, and snack bars is expected to motivate the hemp-based food products market over the forecast period. In addition to this, hemp seeds are rich with amino acids which made these products an ideal choice for health-conscious and vegan consumers. Hemp-based food is emerging as the ultimate source of protein for vegans due to its better digestibility than that of other plant proteins. Apart from this, hemp seeds could be easily added to baking goods or incorporated into salads or soups.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=18113

The hemp-based food market is geographically distributed over North America, Europe, Asia Pacific, Middle East & Africa (MEA), and Latin America. North America held the maximum share in this market in 2015due to a growing consumer preference for healthy food products free of allergens. It was followed by Europe and Asia Pacific. Their gluten-free property has propelled several gluten-sensitive consumers to change their inclination toward these products. Asia Pacific is a highly attractive market, owing to the adoption of Western food habits among this region’s population. Latin America is a potential market with its share likely to rise over the forecast period.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/global-dairy-alternatives-market-to-reach-valuation-of-whopping-us-34-6-bn-by-2029-transparency-market-research-301000215.html

The global hemp-based food market is extremely competitive with the presence of a large number of large-scale and small-scale vendors who compete with each other in terms of product differentiation, quality, price, innovation, distribution, and brand promotion. Key players operating in the market include Hemp co, Naturally Splendid, Mettrum Originals, and Manitoba Harvest. Other prominent ones include Canada Hemp Foods, Braham and Murray, Elixinol, Nutiva, Healthy Brands Collective, Laguna Blends, Hemp Foods Australia, and The Cool Hemp Company. These players dominate the market with their vast geographic presence and large production facilities across different countries. However, the global hemp-based food market is also characterized by the presence of several emerging regional and small manufacturers who lead the market in countries such as the U.K. and China and invest huge amounts of capital in research and development activities and innovation centers in order to expandtheir production capabilities and meet the growing market demands. In addition to this, major players are expanding their market share through new product development, mergers &acquisitions, joint ventures, and expansion, while focusing on their plans to open new retail outlets to strengthen their distribution channels and increase their earnings. In order to meet the growing consumer demands, a variety of different products are launched in the market by various leading as well as emerging manufacturers.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=18113

Coffee Beans Market - Global Industry Analysis, and Forecast 2024

Global Coffee Beans Market: Overview

The global coffee market is expected to rise at a healthy CAGR between the years of 2016 and 2024. The persistently rising consumption of coffee as a daily beverage as led to phenomenal growth of the overall market in recent years. Coffee beans are treated in several ways to sell various types of coffee blends. Internet retailing, growing number of retailers, and direct selling have collectively contributed toward growth of the global market.

The research report studies in the global coffee beans market in complete detail. It uses a SWOT analysis to analyze the strengths, weaknesses, opportunities, and threats influencing the segments of the global market. Furthermore, the research report also includes recommendations and comments by expert market leaders to authenticate the information provided in the research report.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=18500

Global Coffee Beans Market: Drivers and Trends

The global coffee beans market has been growing at a steady pace and is expected to gain momentum in the coming years due to increased consumption of coffee in various parts of the world. The rise of coffee intake across various age groups has led to a high demand for coffee. The research report indicates that the export of coffee accounted to 8.99 million bags in September 2016 from 8.89 million bags in September 2015.

The various types of coffees available in the global coffee beans market are Arabica, Robusta, and others. These coffees are used for personal care, food, dietary supplements, and pharmaceuticals. Analysts expect that the demand for cold coffee is expected to show significant progress across the U.S. and Japan. Strong presence of coffee shop chains such as Peet’s Coffee & Tea and Starbucks have triggered a wave of coffee consumption amongst young population and the working class. Additionally, usage of coffee in production of a wide range of personal care products, baked goods, and chocolates amongst others has also benefitted the global market.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/global-dairy-alternatives-market-to-reach-valuation-of-whopping-us-34-6-bn-by-2029-transparency-market-research-301000215.html

Global Coffee Beans Market: Regional Outlook

In terms of geography, the global coffee beans market is segmented into Latin America, North America, Eastern Europe, Western Europe, the Middle East & Africa, Asia Pacific except Japan, and Japan. The demand for coffee in North America is expected to remain high in the coming years due to an excessive consumption of this brew. The increasing demand for coffee amongst the working population and ubiquitous installment of coffee vending machines at offices, airports, railway stations, and other places are expected to make a generous contribution to the rising revenue of the North America coffee beans market. Furthermore, the spurt of coffee shops in the U.S. and Canada have also spiked the uptake of coffee in recent years.

Asia Pacific is also expected to be a strong contender in the global coffee beans market. Emerging economies such as India and China are expected to be instrumental to the rise of the Asia Pacific coffee beans market. In addition, the market will also be driven by the rising disposable income that is being spent on coffee consumption at coffee shops, growing pool of young population that has been nurturing the coffee-shop culture, and the significantly large coffee plantations that are known to provide some of the best coffee in the world. Latin America too is projected to be an important regional player in the global coffee beans market as the region is known to be the seasoned producer of high-quality coffee beans.

Request For the Customization - https://www.transparencymarketresearch.com/sample/sample.php?flag=CR&rep_id=18500

Key Players Mentioned in the Report are:

Some of the key players operating in the global coffee beans market are Kicking Horse Whole Bean, illy's Medium Roast, Ethiopian Yirgacheffe, Lavazza Super Crema Espresso, Hawaiian Gold Kona Gourmet Blend, Coffee Bean Direct Italian Roast, and others.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=18500

Edible Insects Market - Global Industry Size, Market Share, and Forecast 2024

Global Edible Insects Market: Overview

Edible insects have gone through a huge transition from being famine food to a food included in the daily diet. At present, insects are not just consumed during scarcity of conventional food products but are also part of the food culture of many countries. Edible insects are not only used as human food but also as animal feed due to the presence of amino acids and essential minerals in them.

Edible insects such as ants, wasps, bees, flies, scale insects, termites, cockroaches, crickets, beetles, and grasshoppers are rich sources of nutrition for poultry. By type, the global edible insects market is segmented into beetles, termites, caterpillar, locusts, grasshoppers, mealworm, and others. Based on application the market is classified into animal feed (aquaculture and poultry), human food, and others.

The research report provides an in-depth analysis of the growth trajectory of the global edible insects market and the opportunities that are likely to benefit the vendors of edible insects in future. It evaluates the key segments and highlights their share in the global edible insects market. The report further delves into the competitive landscape of the market and provides information about the degree of barriers to entry and exit in the market by utilizing the Porter’s five forces analysis. The study also presents projections on the volume and revenue growth of the global edible insects market. The dynamics that are likely to restrain or drive the growth of the market are also mentioned in the report.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=10892

Global Edible Insects Market: Trends and Opportunities

The growth of the global edible insects market can be attributed to the increasing demand for food products with high protein value among middle class consumers and the rising population across the world. Feed and food insecurity and the high cost of animal protein are factors that have lifted the consumption of edible insects as feed and food. Entomophagy or consumption of insects is considered to have a positive impact on the livelihood and health of consumers.

The global edible insects market is anticipated to be steered by the growing practice of consuming edible in various local food cultures across the globe. In many developing countries, insects are an important source of food supplement for malnourished children as they can be easily digested. In Europe, the demand for edible insects is considerably high owing to the minimal risk of disease transfer as compared to animals and the presence of micronutrients and nutrients such as fatty acids, zinc, selenium, phosphorus, manganese, magnesium, iron, and copper.

However, the dearth of distribution and networking channels and absence of a legal framework regarding the consumption of edible insects are factors that are likely to inhibit the growth of the global edible insect market. Furthermore, negative perceptions about insect consumption among consumers and lack of awareness are also likely to impede the growth of the market over the forthcoming years.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/global-pet-food-market-to-show-an-impressive-cagr-of-6-from-2019-to-2029-with-valuation-expected-to-reach-us-168-3-bn-finds-tmr-300999294.html

Global Edible Insect Market: Regional Outlook

The global edible insect market is segmented into Europe, Asia Pacific, North America, and the Rest of the World. Asia Pacific emerged as the leading region in terms of consumption of edible insects. Countries such as Sri Lanka, Malaysia, India, Bangladesh, and China are the major consumers of edible insects in the region. The edible insect market in Africa is also expected to witness strong growth owing to the demand for edible insects for nutritional value.

Request For the Customization - https://www.transparencymarketresearch.com/sample/sample.php?flag=CR&rep_id=10892

Companies Mentioned in the Report

Leading companies operating in the global edible insect market are focusing on large scale publicity of their products and innovative packaging for increasing their consumer base. Some of the companies mentioned in the report are HaoCheng Mealworm Inc., Reese Finer Foods Inc., AgriProtein Technologies, Kreca V.O.F., LLC, and EnviroFlight.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=10892

Cocoa Butter Market - Global Industry Analysis and Forecast 2025

Cocoa Butter Market Introduction

Cocoa Butter is a type of vegetable fat and also known as theobroma oil, which is extracted from whole cocoa beans after fermentation and roasting process. Cocoa beans are native to South American countries and one of the largest producers of cocoa is Ivory Coast which is located in Africa. The cocoa butter is used in the production of chocolates, ointments, toiletries, and pharmaceuticals. It is also used for cocoa flavor and aroma of cocoa beans. Cocoa butter helps treat several health issues such as skin irritation, hair loss, and other health issues. It contains flavonoids which have around all sorts of health benefits and because of that it gives a positive impact on the reduction of heart disease, maintains healthy blood pressure, and improve skin conditions.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=33461

Cocoa Butter Market Segmentation

The Cocoa Butter Market can be segmented on the basis of form, types, end-user, packaging, distribution channel and region.

By form, cocoa butter market can be segmented into solid and liquid form. Among the two forms, the solid form is the highest supplied product in the market by the manufacturers and is expected to grow further in the forecast period. Liquid cocoa butter is supplied in tanks while the solid is supplied in blocks, cubes and chips boxes.

By types, cocoa butter market can be segmented into organic, conventional, and deodorized cocoa butter. The organic cocoa butter is made by expeller pressed extraction process, the conventional cocoa butter is made by pure prime pressed extraction process and the deodorized cocoa butter is fully deodorized by a physical process and is mostly used for chocolate production.

By end-user, cocoa butter market can be segmented into food industry, pharmaceutical industry, aromatherapy, cosmetics and personal care industry. In the food industry, cocoa butter is used in the production of confectionery products such as chocolates. In the pharmaceutical industry, cocoa butter is used for its physical properties as cocoa beans are a high-antioxidant in nature since they contain an ample amount of polyphenol and flavonoid antioxidants. It also boosts the immune system, improves heart health, and eases constipation. In aromatherapy, the cocoa butter is used due to its fragrance and natural properties. Cocoa butter is blended with Neroli, which is an essential oil, reflects a fresh scent and helps combat anxiety and depression. In the cosmetics and personal care industry, cocoa butter is used to manufacture lotions, creams, salves, lip balms, hair conditioners, body soaps, and gels. It reduces signs of aging such as wrinkles and hair loss, skin inflammation and removes scars. The cocoa butter also prevents the onset of male pattern baldness.

By packaging, cocoa butter market can be segmented into tins, cartons, plastic containers, paper containers and others. Tin packaging is used for the liquid form of cocoa butter and other packaging for the solid form such as blocks, crystals, and others.

By distribution channel, cocoa butter market can be segmented into direct and indirect sales, which can be further sub-segmented into modern trade units, departmental stores, convenience stores, and online retail.

By region, cocoa butter market can be segmented into five different regions, which includes North America, Latin America, Europe, Asia Pacific, Middle East and Africa. In terms of production, the major regions include Africa, followed by Asia Pacific and Latin America. In terms of consumption, Europe is the largest consumer of cocoa and cocoa butter followed by North America, Asia Pacific, and Latin America.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/global-pet-food-market-to-show-an-impressive-cagr-of-6-from-2019-to-2029-with-valuation-expected-to-reach-us-168-3-bn-finds-tmr-300999294.html

Cocoa Butter Market Drivers, Restraints, and Trends

The Cocoa Butter Market is been growing gradually based on its medicinal and nutritional benefits. Recently people are adapting traditional products due to rising health concern, and also because of the harmful side effects of chemicals. Cocoa beans are one of the oldest ingredients which are preferred by manufacturers for the main production of all types of chocolates, by consumers for its medicinal and nutritional uses. Cocoa butter is extracted from cocoa beans and it is rich in calories, saturated fats, palmitic acid, stearic acid and oleic acid. Cocoa butter is used to prevent skin dryness and peeling, heals chapped lips, fights signs of aging, soothes burns and infections, and helps treating mouth sores, helps improve heart health, and raises immunity. It increases concentration among people and eliminates stress and exhaustion. All these benefits of cocoa butter are making it popular among people and driving the cocoa butter market in the developed as well as developing regions.

Besides several benefits of nutmeg butter, it has various side-effects too. Over intake of cocoa butter can lead to weight gain and obesity, allergy and skin reactions, cholesterol, heart and respiratory problems. These side effects are therefore inhibiting the cocoa butter market to grow.

Request for Custom Research at - https://www.transparencymarketresearch.com/sample/sample.php?flag=CR&rep_id=33461

Cocoa Butter Market Key Players

Owing to the benefits of cocoa butter, several producers and players in the market are moving forward to manufacture and supply it. Some of the key players are Cargill Incorporated., Cocoa Mae, Chocolate Alchemy, Dietz Cacao Trading B.V., Jindal Cocoa, Carst & Walker (C&W), JB FOODS Limited and others.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=33461

Magnesium Hydroxide Market - Global Industry Analysis, and Forecast 2026

Global Magnesium Hydroxide Market: Overview

Magnesium hydroxide is defined as an inorganic compound obtained by precipitation process between the magnesium salts and sodium, or potassium and ammonium hydroxide. Brucite, which is a form of natural magnesium, is used for commercial purposes such as fire retardant while most industrially used magnesium hydroxide is produced synthetically. Brucite may also crystallise in cement and concrete in contact with seawater. Magnesium hydroxide has chemical formula of Mg(OH)2. Commercial and industrial magnesium hydroxide is chemically manufactured from seawater or brine. Magnesium hydroxide is known as milk of magnesia owing to its milk-like appearance. This compound is less soluble in water. It possesses properties such as flame retardancy, low corrosiveness, and low toxicity.

Download PDF Brochure – https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=48897

Global Magnesium Hydroxide Market: Drivers and Restraints

Rise in usage of magnesium hydroxide in industries such as pharmaceutical and healthcare owing to its specific properties is propelling the magnesium hydroxide market. Magnesium hydroxide is employed in antiperspirant deodorants, which is used on a large scale by the young generation population. This is augmenting the magnesium hydroxide market. Magnesium hydroxide is also used in fossil-fuel based power plants during the process of desulfurization. This is another factor driving the magnesium hydroxide market. Increase in usage of magnesium hydroxide in the water treatment industry is also boosting the magnesium hydroxide market. On the other hand, implementation of government regulations on the usage of magnesium hydroxide in the food industry is hampering the magnesium hydroxide market. Side effects such as allergic reactions, skin rashes, itching, and loss of appetite are also hindering the magnesium hydroxide market.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/valuation-of-global-3d-printing-materials-market-to-climb-to-us-9-5-bn-by-2027-demand-for-3d-printed-products-in-diverse-industries-reinforce-prospects-tmr-301086699.html

Global Magnesium Hydroxide Market: Key Segments

Based on the grade type, the magnesium hydroxide market can be segmented into retardant grade, industrial grade, and pharmaceutical grade.

In terms of end-use industry, the magnesium hydroxide market can be divided into rubber, building materials, magnesium salt, and activated magnesium oxide.

Based on geography, the magnesium hydroxide market can be segregated into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. North America dominates the market in terms of revenue owing to the increase in adoption of magnesium hydroxide in chemical, oil, food, and water industries. The market in North America is followed by that in Europe in terms of value. The magnesium hydroxide market in Asia Pacific is expected to expand at a rapid pace during the forecast period owing to the rise in adoption of magnesium hydroxide in the building & construction industry.

Request For the Customization - https://www.transparencymarketresearch.com/sample/sample.php?flag=CR&rep_id=48897

Global Magnesium Hydroxide Market: Key Players

Key players operating in the magnesium hydroxide market include Nedmag Industries Mining & Manufacturing B.V., Nabaltec AG, Huber Engineering Materials, Kyowa Chemical Industry Company Limited, Konoshima Chemical Company Limited., Tateho Chemical Industries Company Limited, and Baymag Inc., Akzo Nobel N.V., Albemarle Corporation, Almatis GmbH, BASF SE, Chemtura Corporation, China Minmetals Nonferrous metals, Cyter Industries, Israel Chemicals etc.

The report offers a comprehensive evaluation of the market. It does so via in-depth qualitative insights, historical data, and verifiable projections about market size. The projections featured in the report have been derived using proven research methodologies and assumptions. By doing so, the research report serves as a repository of analysis and information for every facet of the market, including but not limited to: Regional markets, technology, types, and applications.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=48897

Coiled Tubing Market - Global Industry Analysis, and Forecast 2019

Coiled tubing is used in the Oil and Gas industry, primarily for upstream activities. It is a lengthy and coiled tubular product used for oil and gas well operations. It also finds use in well clean out’s, pumping of nitrogen and as production tubing in depleted gas wells among others. Coiled tubing services are divided into well intervention services, drilling services and other services.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=2127

The usage of coiled tubing in the oil and gas industry has multiple advantages ranging from contained well pressure, quicker trip times and lower personnel requirement among others. The market is poised for growth as more and more investments are being channeled towards the E&P industry. With development of offshore and deep-water drilling markets picking up the usage of such coiled tubing in these markets are imminent. Extensive shale gas exploration and drilling activities all over the world is one of the primary drivers of this market. Growing energy demands are likely to sustain the drilling industry even in the distant future and ensure the demand for such coiled tubing’s.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/global-solar-street-lighting-market-to-reach-a-valuation-of-us-12-54-bn-by-2027-the-renewable-energy-movement-to-drive-solar-street-lighting-market-finds-tmr-301028795.html

The coiled tubing market can be segmented on basis of services as well intervention services, drilling services and other services. Well intervention services can be segmented into well cleaning and well completion services (acid & chemical treatment, fishing, logging and perforation etc.). On the regional front North America is currently the largest market for coiled tubing both in terms of value and active fleet count. As awareness regarding benefits of this technology is increasing, other world markets are likely to increase their demand for coiled tubing. An expanding scope of business has been observed in areas like Europe, Asia Pacific and the Middle Eastern regions. However with the slowdown in North-American demand the overall growth curve for the industry is likely to be moderated in the near future.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=2127

Some of the key players in the industry are Schlumberger Ltd, Halliburton Co, Trican Well Services Ltd, Superior Energy Services Inc, Calfrac Well Services Ltd and Baker Hughes Inc. among others.

Bio-based Construction Polymers Market - Global Industry Analysis and Forecast 2025

Bio-based polymers are materials manufactured from renewable resources. They are highly preferred in construction applications due to the rise in demand for non-fossil fuel based polymers. Earlier, bio-based polymers would be derived from agriculture feedstock such as potatoes, corn, and other carbohydrate feedstock. However, advancement in bio-technology led to the production of bio-based polymers through the bacterial fermentation process from renewable resources such as starch, cellulose, fatty acids, and organic waste.

Increase in environmental concerns across the world has boosted the usage of bio-based polymers, as they majorly contribute toward reducing the dependency on fossil fuels. This, in turn, helps lower carbon dioxide footprints. Rise in R&D activities for the development of eco-friendly products has accelerated the use of bio-based polymers in construction. Furthermore, implementation of favorable government regulations and initiatives in various countries for the usage of bio-based polymers has been augmenting the market since the last few years. Bio-based polymers are not entirely endowed to gain the advantage of economies of scale. Therefore, high production cost is anticipated to inhibit the market growth during the forecast period.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=33527

The bio-based construction polymers market can be segmented based on type, application, and region. Epoxies, cellulose acetate, polyurethanes (PUR), polyethylene terephthalate (PET), polyethylene (PE), and others are among the major types of bio-based construction polymers. The others category comprises polylactic acid (PLA), polyamides (PA), polytrimethylene terephthalate (PTT), polybutylene succinate (PBS), and starch blends. The epoxies segment is anticipated to account for major share of the bio-based construction polymers market during the forecast period due to its wide range of applications such as wood & concrete repair, adhesives, and paints & coatings. Significance of insulation in the construction industry is likely to drive the polyurethane segment during the forecast period. PLA acts as a pre-foaming agent, binder, suspending agent, foaming agent, and coating adhesive that offers added advantage. This is estimated to propel the segment during the forecast period.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/bioplastic-textiles-market-to-reach-valuation-of-us-1-2-bn-by-2027-popularity-of-green-and-biodegradable-materials-to-drive-demand-within-the-global-market-finds-tmr-301027371.html

Prominent applications of bio-based construction polymers include pipe, insulation, profile, and others. The others segment includes FRP bridge section, concrete molds, glazing sealants, cladding panels, and anchor fixings. The pipe segment constitutes key share of the market, led by the lightweight, durability, and corrosion resistance properties of bio-based construction polymers. These polymers are typically used in construction applications such as building panels, roofing, sealants & adhesives, and flooring. Rise in usage of profiles and frames produced from bio-based polymers in bridge engineering and other composites structures is projected to propel the bio-based construction polymers market during the forecast period.

Request for Discount on This Report at - https://www.transparencymarketresearch.com/sample/sample.php?flag=D&rep_id=33527

In terms of geography, Asia Pacific is anticipated to lead the global bio-based construction polymers market. Middle East & Africa is also expected to offer significant opportunities to the bio-based construction polymers market owing to the increase in construction activities and infrastructural growth in the region. Furthermore, implementation of favorable government regulations and policies is projected to augment the building & construction industry in the region. The bio-based construction polymers market in North America and Europe is estimated to expand at a moderate pace due to the less number of construction activities vis-à-vis those in emerging economies.

The bio-based construction polymers market is in the nascent stage. Thus, it is considered to be highly competitive. The market is dominated by large players. Various development strategies such as mergers & acquisitions, joint ventures, and new product launches are likely to be implemented during the forecast period.

Key players operating in the bio-based construction polymers market include E. I. du Pont de Nemours and Company (the U.S.), Covestro (Germany), BASF SE (Germany), Bio-On SpA (Italy), Kaneka Corporation (Japan), .

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=33527

Automotive Glass Market - Global Industry Analysis, and Forecast 2023

Global Automotive Glass Market: Overview

Different types of glasses are used for the manufacturing of an automobile, such as windshield, glass panel roof, and side and rear windows. These are collectively called as automotive glass. Advanced windshields available these days not only block the wind as well as other flying debris from entering the fast moving vehicle, they are designed aerodynamically to breach the air swiftly. Moreover, laminated safety glass now exhibit spiderweb cracking, which adds to the protective aspects in case of accidents. With the rise in global population and increasing disposable income, the automotive industry is thriving and concurrently, the demand in the global automotive glass market is expected to escalate at a robust CAGR during the forecast period of 2016 to 2024.

This report on global automotive glass market is a thorough study, aimed to act as knowledgebase for the players in making more informed decisions. The report provides an analysis of all the factors that may impact the demand during the forecast period, besides highlighting some of the key trends. It also profiles some of the key players for their market share, product portfolio, and recent developments. The global automotive market can be segmented on the basis of product type, application, end-use, vehicle type, and geography. By product type, the market can be divided into tempered, laminated, and others while by application, the market can be segmented into windshield, sidelite, and backlite. By end-use, the market can be categorized into original equipment manufactured (OEM) and aftermarket auto glass (ARG), while by vehicle type, the segments can be passenger car, light commercial vehicle, and heavy commercial vehicle.

Download PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=7445

Global Automotive Glass Market: Trends and Opportunities

The automotive glass industry is expected to gain from the increasing global GDP and rapid urbanization across the emerging economies. The demand in the overall automobile industry is at its peak and consumers are now willing to spend extra for quality products. The report identifies side glazing as the latest trend in the automotive glass market, which is anticipated to increment the average glass used per vehicle. With the increasing awareness among the end users pertaining to security and safety offered by advanced products, the research and development is being carried out by the players in automotive glass manufacturers. Photochromic properties offered by advanced glasses that considerably reduce the intensity of ultraviolet (UV) radiation and automotive smart glass with auto dimming properties are two such innovation that has been well received by the end-users. The smart glass segment of automotive glass optimizes the experience by manipulating natural light, lighting load, and cooling and heating load.

Currently, tempered automotive glass product segment dominates the market, although laminated glass is projected for a significantly higher growth rate during the forecast period. By application, windshield serves the maximum demand in global automotive glass market while by end-use, OEM leads over ARG on account of vehicle safety features from the manufacturing end. By type of product segment, passenger cars account for the lion share of the market.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/animal-feed-amino-acids-market-to-reach-valuation-of-us-14-1-bn-by-2027-developing-concerns-about-animal-health-stimulates-the-growth-of-global-market-noted-tmr-301026065.html

Global Automotive Glass Market: Region-wise Outlook

Geographically, the report divides the market into North America, Europe, Asia Pacific, and rest of the world. Currently, Asia Pacific serves the maximum demand, owing to factors such as availability of cheap and skilled labor, which is enticing foreign investments in the region. North America is also expected to witness consistent growth due to increase in the manufacturing of commercial vehicles in the developed countries of the U.S. and Canada.

Request for Discount on This Report at - https://www.transparencymarketresearch.com/sample/sample.php?flag=D&rep_id=7445

Companies mentioned in the research report

Fuyao Group Automobile Glass Co., Ltd., Asahi Glass Company, Saint Gobain, Nippon Sheet Glass Co., Ltd., Magna International, Xinyi Glass, and Gentex Corporation are some of the key companies in the global automotive glass market, wherein top four companies reserve dominant share. Investments for research and development of new products and expansion of the manufacturing capability are two common strategies adopted by the market players to gain shares. For example, AGC invested US$163.2 million in March 2016 to manufacture the second float glass manufacturing facility in Brazil. It is likely to get completed by 2018.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=7445

Hydraulic Fracturing Market - Industry Analysis, Size, Share, Forecast 2022

Transparency Market Research (TMR) has published a new market study based on the global hydraulic fracturing market. With an increase in the number of successful discoveries of shale gas and tight gas reserves, hydraulic fracturing (fracking) techniques are adopted extensively to extract large quantities of hydrocarbons. The global hydraulic fracturing market valued at US$38.32 bn in 2014 and is expected to reach US$66.06 bn by 2022, expanding at a CAGR of 6.12% in the period from 2014 to 2022. The report is titled “Hydraulic Fracturing Market, - Global Industry Analysis, Size, Share, Growth Trends, and Forecast 2014 - 2022.”

Browse the full Hydraulic Fracturing Market, by Technology (Plug and Perf and Sliding Sleeves) and by Application (Conventional, Shale Gas, and Others) - Global Industry Analysis, Size, Share, Growth Trends, and Forecast, 2014 - 2022 report at https://www.transparencymarketresearch.com/hydraulic-fracturing-market.html

The report states that the hydraulic fracturing market which stood at 21.34 MHHP in 2013, is expected to expand at a CAGR of 5.30% from 2014 to 2022, to reach 33.97 MHHP by 2022 in terms of volume. The report contains an executive summary comprising a snapshot of the hydraulic fracturing market, containing detailed information on the various segments, as well as the market dynamics such as growth drivers and restraining factors. It also analyzes the impact of these dynamics on the market during the forecast period 2014 to 2022.

Hydraulic fracturing techniques are primarily implemented on unconventional reservoirs such as tight oil, tight gas, shale gas, shale oil, and coal bed methane. Over time, hydraulic fracturing has begun to gain preference in conventional gas and oil fields on abandoned wells which were deemed uneconomical in the past. With the implementation of the hydraulic fracturing technique, the production of natural gas and crude oil has become possible from matured fields. Currently, 70% of the overall production of hydrocarbons is from matured fields.

More Trending Reports by Transparency Market Research -https://www.prnewswire.com/news-releases/liquid-biofuel-market-to-reach-valuation-of-us-295-bn-by-2027-depleting-conventional-fuel-reserves-has-led-the-manufacturers-to-develop-effective-biofuels-opines-tmr-301025344.html

The application of hydraulic fracturing techniques results in significant cost and time savings, which is one of the reasons for an increase in the adoption of this technique. The adoption of hydraulic fracturing by several countries such as Saudi Arabia, Oman, and the U.S. for both conventional and unconventional gas and oil fields has propelled the global hydraulic fracturing market. Moreover, according to the U.S. Energy Information Administration (EIA), large quantities of shale gas and shale oil reserves are available for extraction in North America, which will further drive the hydraulic fracturing market. These discoveries in North America have helped the region to transform from an energy importing nation to an energy exporting nation. It has also helped the region to create huge employment opportunities and increase energy security. According to the report, North America would be the largest exporter of natural gas and crude oil in the future, indicating many emergent opportunities in the fracking market in North America.

The global hydraulic fracturing market is segmented on the basis of technology, application, and region. Major regions studied are Europe, North America, Asia Pacific, and RoW. Out of these, North America dominates the market, owing to large shale reserves present in the region. On the basis of application, the market is segmented into conventional, shale gas, and others.

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=587

Key players in the hydraulic fracturing market include: Calfrac Well Services Ltd., Baker Hughes Inc., FTS International, Inc., Nabors Industries Ltd., RPC, Inc., Halliburton Company, Schlumberger Limited, Trican Well Services Limited, Weatherford International Ltd, and United Oilfield Services, Inc.

Ginger Market - Global Industry Report, 2022

The global reach and acceptance for spices, especially for ginger have been increasing in recent years, presenting promising growth opportunities for large-scale manufacturers and processors of the spice that also promises vast health benefits, observes Transparency Market Research in a recent report. The global ginger market has multiple players, owing to which the vendor landscape is fragmented and is competitive in nature. The dominant players in the global ginger market are Yummy Food Industrial Group, Sun Impex International Foods L.L.C., Archer-Daniels-Midland Co., Indian Organic Farmers Producer Co. Ltd., Monterey Bay Spice Co. Inc., Buderim Group Ltd., SA Rawther Spices Pvt. Ltd, Atmiya International, Food Market Management Inc., and Sino-Nature International Co. Ltd.

According to the report, the global ginger market is expected to reach a valuation of US$4.18 bn by the end of 2022; the market is expected to expand at a 6.5% CAGR during the forecast period of 2017 to 2022.

Request Sample pages of premium Research Report - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=33065

Asia Pacific to remain the Leader in Global Ginger Market

The report segments the global ginger market t based on the form of ginger into fresh, pickled, dried, preserved, powdered, and crystallized. Among all these forms, fresh ginger is the most preferred market form. The segment presently accounts for the dominant share in terms of valuation in the overall market and is expected to exhibit a CAGR of 7.30% over the report’s forecast period. Global ginger market is further segmented on the basis of application, distribution channel and region.

Geographically, Asia Pacific excluding Japan (APEJ) is the leading regional market. It is expected to expand at a CAGR of 7.10% over the forecast period. In the Asian market India and China are drawing enormous amount of medical tourism for which ginger is a key medical spice. Thus, the rise in medical tourism activities has provided a significant push for the APEJ market and is likely to remain a key growth factor for the regional market over the forecast period as well. Other regions are also making effective measures to increase the production of spices, especially ginger, with the increasing medical awareness regarding organic substances.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/dietary-supplement-providers-harness-omega-3-ingredients-market-to-expand-portfolio-global-market-to-garner-cagr-of-11-from-2019-to-2027-transparency-market-research-301002842.html

Multi-remedial Nature of Ginger allows its Increased Adoption

The global ginger market has gained immense popularity in the recent years as the spice helps in curing multiple diseases like cancer, nausea, cardiovascular diseases and diabetes. Apart from being a remedy form regular infections like cold and cough, it also helps in improving indigestion, arthritis, rheumatism, hypertension, constipation, ulcers, and atherosclerosis. Therefore the global ginger market is projected to enjoy the advantage of a number of positive factors to increase demand in the foreseeable future. In the coming years, the ginger market is expected see a steady expansion in its application base from medicine to alcohol and beverages, which will boost the overall consumption of ginger globally. The information presented in this review is based on a TMR report, titled “Ginger Market (Form - Fresh, Dried, Pickled, Preserved, Crystallized, and Powdered; Distribution Channel - Modern Grocery Retail, Traditional Grocery Retail, and Non-Grocery Retail; Application - Culinary, Soups and Sauces, Snacks & Convenience Food, Bakery Products, Alcoholic Beverages, Non-Alcoholic Beverages, and Chocolate and Confectionery) - Global Industry Analysis, Size, Share, Growth, Trends and Forecast 2017 - 2022.”

Request for covid19 Impact Analysis - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=33065

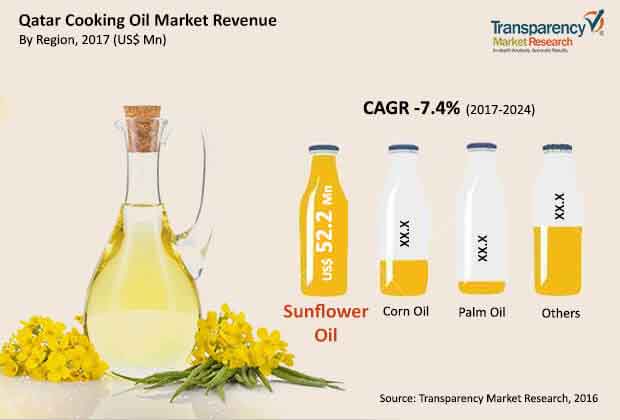

GCC Cooking Oil Market - Global Industry Report, 2023

The GCC and Qatar cooking oil market is recognized as a compact matrix of consolidated key companies. Organizations such as United Food Company, Savola Group, and Emirate Refining Company are some of the key players of the matrix of GCC and Qatar cooking oil market. Altogether, these organizations acquire at least 75% of the market share by the end of 2015. In a market where the competition is extremely intense, many other companies are aggressively conducting research and development so as to introduce new product lines of nutritious cooking oils. In order to sustain the tough competition organizations are investing heavily in promotional activities so as to extend their knowledge about their new products and launch them with lavishly.

As per the market study conducted by Transparency Market Research (TMR), the GCC and Qatar cooking oil market is projected to grow at a staggering CAGR rate of 6.6% and 7.4% respectively from 2017 to 2024. At this rate, the GCC cooking oil market is to jump to $1736.1 million from $1103 million in the forecast tenure. On the other hand, Qatar cooking oil market is projected to translate the CAGR growth into $122.2 million in the projected forecast period.

The GCC cooking oil market is segmented into various facets. By product type, the market is fragmented into sunflower oil, corn oil, and palm oil. Out of these segments, the sunflower oil segment tops every other cooking oil market segment. The reason that this segment exceeds other segments owing to its rising health concerns amongst end-users. Likewise, the Qatar cooking oil market is bifurcated on the basis of product type, package, and region. The market is expected to be owned by sunflower oil with a market share of 71.5% in terms of revenue in forthcoming years.

Region wise the GCC is likely to excel better than other regions. This growth will be the outcome of a large number of immigrants from countries like India and Sri Lanka, where cooking oil is extensively used in their traditional cooking.

Request Sample pages of premium Research Report - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=15008

What are The Major Growth Drivers of Cooking Oil Market in GCC and Qatar?

The major driving factor of the growth of the cooking oil market in GCC and Qatar is the increasing demand for processed food. Extensive consumption of oil-based packaged food is yet another factor that drives the growth of GCC and Qatar cooking oil market. In order to fulfill this rising demand in the region, manufacturers are conducting various research and development activities. The changing lifestyle of the people and increasing disposable income of the public tends to change the eating habits of the people in the region. This yet again leads to the strengthening of GCC and Qatar cooking oil market.

On the other hand, rising tourism is playing a crucial role in the growth of cooking oil market in GCC and Qatar. As this influx of tourist bodes effectively for hospitality sector along with ancillary industries. This rising tourism has drawn attention of various hotel chain in the region from various region of the world. This in turns supports the growth of GCC and Qatar cooking oil market.

More Trending Reports by Transparency Market Research - https://www.prnewswire.com/news-releases/global-dairy-alternatives-market-to-reach-valuation-of-whopping-us-34-6-bn-by-2029-transparency-market-research-301000215.html

What Restrains the Growth of GCC and Qatar Cooking Oil Market?

Since the region shows exception growth in the future, every big fish wants to grab the opportunity. However, factors such as minimal production locally owing to the harsh climatic conditions and major political instability, the growth of GCC and Qatar cooking oil market gets hampered. The above-mentioned reasons lead to high dependency over imports again playing a crucial role in hampering the growth of the cooking oil market in GCC and Qatar.